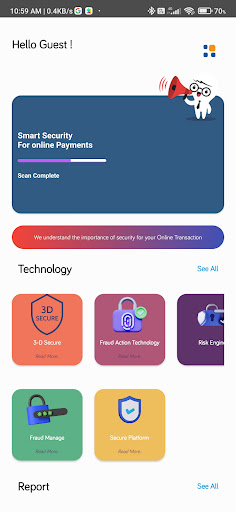

Features Pavika Payment Safety

Payment safety refers to the measures and protocols in place to secure financial transactions and protect sensitive payment information from unauthorized access, theft, or fraud.

Ensuring payment safety is crucial in online and offline transactions to safeguard both consumers and businesses.Payment safety measures include encryption technologies, secure payment gateways, and two-factor authentication.

Online retailers and service providers often employ SSL (Secure Sockets Layer) certificates to encrypt data transmitted between the users browser and the website, ensuring that payment details remain confidential.Additionally, financial institutions implement real-time fraud detection systems that analyze transaction patterns and flag suspicious activities.

Consumers can enhance payment safety by using secure, unique passwords, regularly monitoring their accounts, and avoiding public Wi-Fi for sensitive transactions.Payment safety is a critical aspect of any financial transaction, ensuring that sensitive information is protected from unauthorized access, fraud, and theft.

Various measures are implemented to guarantee payment safety, especially in online transactions.

These measures include encryption technologies, secure payment gateways, and multi-factor authentication methods.[1] Encryption Technologies: Online platforms use SSL (Secure Sockets Layer) and TLS (Transport Layer Security) encryption protocols to secure data transmission between users and websites, making it difficult for hackers to intercept sensitive information.[2] Secure Payment Gateways: Reliable payment gateways act as intermediaries between merchants and customers, ensuring secure payment processing.

These gateways employ advanced security protocols to safeguard payment data during transactions.[3]Multi-Factor Authentication (MFA): MFA adds an extra layer of security by requiring users to provide multiple forms of identification before accessing their accounts.

This can include something the user knows (password), something they have (a security token), or something they are (biometric data).[4]Regular Security Updates: Both payment service providers and consumers must keep their software, applications, and devices updated to patch security vulnerabilities promptly.[5]Vigilant Monitoring: Financial institutions often employ real-time monitoring systems to detect unusual activities and potential fraud, allowing for immediate intervention when necessary.

News & Updates

Stay informed with the latest news and updates.

Smart Home

Control and monitor your home with smart features.

Offline Mode

Use the app without an internet connection. Your data syncs when you're back online.

See the Pavika Payment Safety in Action

Get the App Today

Available for Android 8.0 and above